Your credit score in the United States is one of the most important numbers that affects almost every aspect of your financial life. Whether you’re renting an apartment, applying for a credit card, getting a car loan, or even seeking certain jobs, your credit score plays a critical role.

If you are new to the U.S., a student, an immigrant, or someone starting their financial journey, understanding how credit scores work can save you money, stress, and unnecessary financial mistakes.

At USAHarmony, we regularly answer real questions from beginners and first-time credit users across the U.S.This guide is written in simple, USA-English, with step-by-step instructions, examples, and tips you can implement right away.

What Is a Credit Score?

A credit score is a three-digit number representing your financial reliability as a borrower. Lenders use it to decide:

Whether to approve loans or credit cards

The interest rate you will be charged

The amount of credit limit you are eligible for

Credit scores in the U.S. generally range from 300 to 850. The higher your score, the lower the perceived risk, which translates into better loan terms and lower interest rates.

At USAHarmony, we often see beginners underestimate the importance of their credit score. Even a minor mistake, like missing a payment, can affect your financial life for years.

Major Credit Bureaus in the USA

Credit scores are calculated using information collected by three main credit bureaus:

Experian

Equifax

TransUnion

Each bureau collects your financial activity, including loans, credit cards, and bill payments, and creates your credit report. While your scores may vary slightly between bureaus, the differences are usually minor.

Tip: Checking your credit report from all three bureaus annually is a good habit to ensure accuracy.

Popular Credit Score Models

Two widely used credit scoring models dominate in the USA:

FICO Score: Used by most banks and lenders to assess creditworthiness.

VantageScore: Commonly used by free credit apps and some lenders.

Both scoring models weigh your financial behavior similarly, though percentages can differ slightly.Understanding which scoring model your lender uses can help you focus on areas that matter most.

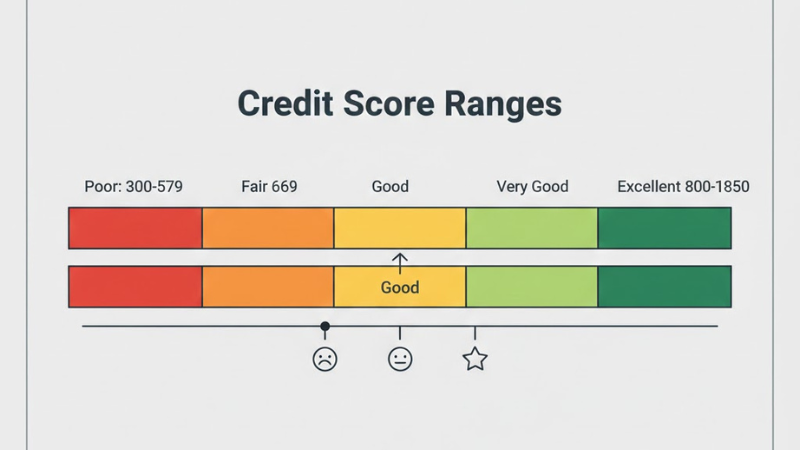

Credit Score Ranges Explained

| Credit Score | Meaning |

|---|---|

| 300–579 | Poor |

| 580–669 | Fair |

| 670–739 | Good |

| 740–799 | Very Good |

| 800–850 | Excellent |

Reaching a score of 670 or above is a strong milestone for beginners. Scores above 740 open access to the best credit cards, loans, and financial products.

According to myFICO (https://www.myfico.com/credit-education/credit-scores), a score above 670 is generally considered good.”

Real-life tip: Many beginners start with a “Fair” credit score but can reach “Good” in 6–12 months with discipline.

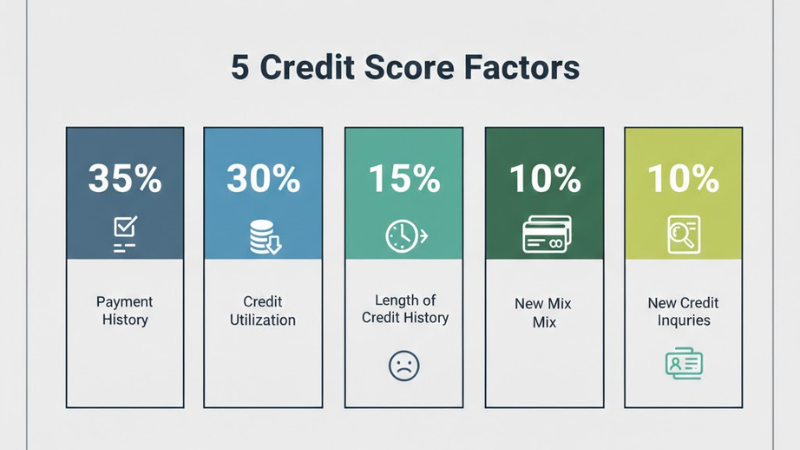

How Credit Scores Are Calculated

1. Payment History (35%)

The most important factor is whether you pay your bills on time. Late payments, collections, or defaults have a major negative impact. Even a single missed payment can drop your score significantly.

2. Credit Utilization (30%)

This measures how much of your available credit you are using.

Example: If your credit limit is $1,000 and you are using $300, your utilization is 30%.

Best practice: Keep utilization below 30%, ideally below 10%.

3. Length of Credit History (15%)

Older accounts help your score.Beginners usually have lower scores because their accounts are new.

4. Credit Mix (10%)

This factor considers the types of credit you use:

Credit cards (revolving credit)

Auto loans

Student loans

Mortgages

A healthy mix can slightly improve your score over time.

5. New Credit Inquiries (10%)

Each time you apply for new credit, a hard inquiry is made. Too many in a short period can reduce your score.

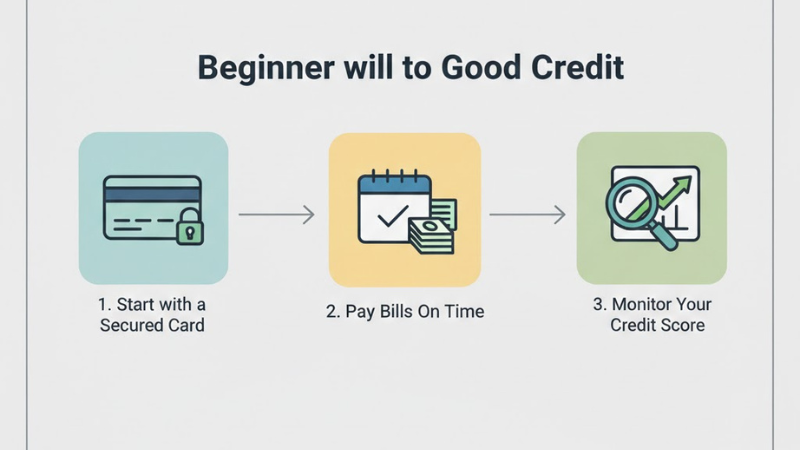

How to Build Credit From Zero

1. Get a Secured Credit Card

A secured credit card requires a refundable deposit and works like a regular credit card. This is often the easiest way to start building credit for beginners.

2. Become an Authorized User

Ask a trusted friend or family member to add you as an authorized user on their credit card. Their good payment history will positively affect your score.

3. Pay Bills on Time, Every Time

Set up automatic payments for minimum balances to avoid late payments. Consistency is key.

4. Keep Credit Usage Low

Avoid maxing out your credit limit. A low utilization rate demonstrates responsible credit behavior.

5. Open a Small Personal Loan

A small installment loan that is repaid on time can help establish credit diversity.

Example:

A new international student opens a secured credit card with a $500 deposit.

They spend $50–$70 monthly and pay on time.

After 6 months, their credit score reaches ~680.

How to Improve Your Existing Credit Score

https://usaharmony.com/finance-open-bank-account-usa/Even if you already have credit, you can improve your score:

Pay down high balances to reduce utilization.

Avoid opening too many accounts at once.

Keep old accounts open to improve credit history length.

Check your credit report regularly for errors.

Maintain a healthy bank account (internal link to /finance/open-bank-account-usa/).

Maintaining strong financial habits is the fastest way to achieve excellent credit over time.

Common Credit Score Mistakes Beginners Make

-

Missing due dates

-

Closing old accounts too early

-

Applying for many cards at once

-

Using full credit limit constantly

-

Ignoring credit reports

Avoiding these mistakes saves years of effort and prevents unnecessary damage to your financial profile.

How Long Does It Take to Build or Improve Credit?

First score appears: 3–6 months

Good score (670+): 6–12 months

Very good score (740+): 12–24 months

Credit building is gradual. Consistency and patience are crucial.

How to Check Your Credit Score for Free

You can check your credit score without lowering it through:

Bank apps

Free credit monitoring services

Annual credit report websites

Checking your own score does not hurt it

“You can get a free copy of your credit report every year from the official AnnualCreditReport.com website.”

External link suggestion:

Consumer Financial Protection Bureau – Check Credit Reports

FAQs: Credit Score in the USA

Yes. 700 is considered good and qualifies for most loans.

Yes. You can start with secured credit cards or by becoming an authorized user.

No. Debit card usage does not affect your credit score.

Some rent-reporting services can help, but it depends on the landlord or service.

Final Thoughts

Building and improving your credit score in the USA is a journey. Start early, follow disciplined financial habits, avoid mistakes, monitor your credit reports, and stay consistent. A strong credit score unlocks better interest rates, improved loan eligibility, and smoother financial life in the U.S.