And then, you know, you’ve just been working very hard to accumulate $1000, or you know, it just lands in your lap like free money. And then you’re just wondering, “What now?” You know, you could waste it, I’m not going to lie. But you’re looking for something a little more viable. You know, the nice thing about having $1000 is that you don’t even have to think about just credit or just investing—you can think about having it all. And then, I guess, it’s not as simple as just doing either-or.

The good news? Well, within my own experience in helping individuals who were just beginning, I have found that one of the biggest things is that, essentially, beginner’s errors are just so commonplace. I mean, I’ve literally seen individuals struggle to figure things out, wasting time, money, effort, and so forth, but in fact, I always want to provide individuals with some good points to keep in mind: provided with the $1000, individuals can in fact set themselves up in pretty good shape, but only if they can get a little bit of a game plan in place.

What is a Secured Credit Card?

Okay, first let’s talk about secured credit cards. If you’ve never used credit before, or if your credit’s a bit of a mess, a secured card is a good starting point. It’s not going to fix your credit overnight, but it’s an option. Basically, you deposit money with the bank-say, $500-and that acts as your “limit” on the card. So you get a card with a $500 limit-but you’ve already paid it.

But the real trick here is making sure not to screw it up by maxing it out. Believe me, people do that. They think, “Oh, it’s just $500; no biggie,” then spend more than they ought to, and that really sets them back. I have seen it happen one time too many. However, if you use the card for small purchases and pay it off every month, you’ll be in good shape.

This is about proving that you can handle credit-not getting free things. Once your credit starts getting better, you may even be able to get a regular credit card. But that takes time. It doesn’t happen overnight.

Check out Secured Credit Cards for more info from Experian.

How to Build Credit with $1000 Using a Secured Credit Card

Building credit with $1000 sounds pretty straightforward, right? Just open a secured card, make some purchases, pay it off. Boom, done. But—here’s the thing—it’s not that easy. It takes time. A lot of people get impatient. It takes about 6 to 12 months to really see some improvement in your credit score. I’ve seen beginners get frustrated and give up long before they start seeing results. But stick with it, and you’ll get there.

Real-Life Scenarios of Building Credit

Now, let’s look at a couple of real-world examples. These aren’t perfect situations. Honestly, there’s always something a little messy about starting out with credit. I’ve watched a lot of people make mistakes, but that’s part of learning. Here are two common scenarios:

Scenario 1: Sarah’s Credit-Building Journey

Sarah had just moved to the U.S. and had no credit history. She opened a Capital One Secured Credit Card with $500. She didn’t go overboard; she bought groceries and maybe a few other small things. The key? She paid her balance every single month. It wasn’t glamorous, but after 6 months, Sarah saw her score improve by about 50 points. It wasn’t huge, but it was something. She felt stuck for a while, but after a year, she was able to get approved for an unsecured credit card.

Scenario 2: John’s Financial Rebuild

John was fresh out of college, and like most young people, his credit history was pretty much a blank slate. He opened a Discover it® Secured Credit Card with $1000. Like Sarah, John used the card for small things, made his payments, and after about 12 months, he noticed his credit score improve enough to get approved for a car loan with a reasonable interest rate. Not a bad deal, right? But the whole process took time. John’s biggest mistake? He wasn’t careful at first and almost maxed out his card. Glad he caught that before it was too late.

For more info on credit building, check out CFPB’s Credit Card Guide.

The Power of $1000: How Investing Early Pays Off

Alright, let’s move to the good stuff: investing. Honestly, it can be a little intimidating to start investing, especially if you’ve never done it before. But here’s the thing: $1000 is enough to start growing your wealth. The earlier you start investing, the more you benefit from compound interest.

So, you’ve probably heard that term before, but let’s talk about what it actually means. Compound interest is when your returns (interest, dividends, etc.) start earning interest themselves. And that can be a game-changer. The longer you leave your money invested, the more it grows.

Compound Interest Example: The Power of Patience (Based on a one-time $1,000 investment)

| Investment Type | Avg. Annual Return | Value after 10 Years | Value after 20 Years |

|---|---|---|---|

| S&P 500 (Index Fund) | ~10% | $2,593 | $6,727 |

| High-Yield Savings (HYSA) | ~4.0%* | $1,480 | $2,191 |

| Cash (Under Mattress) | 0% | $1,000 | $1,000 |

Note: Returns are based on historical averages. Savings rates fluctuate with the economy, and stock market returns are not guaranteed.

This table might not blow your mind, but it tells the story of why it matters to start early. You see, $1000 invested in the S&P 500 Index Fund could grow to $6,727 over 20 years. That’s not magic, that’s compound interest at work. You don’t need to do anything special—just leave it alone. But here’s the thing: it won’t happen overnight.

Learn more about Compound Interest.

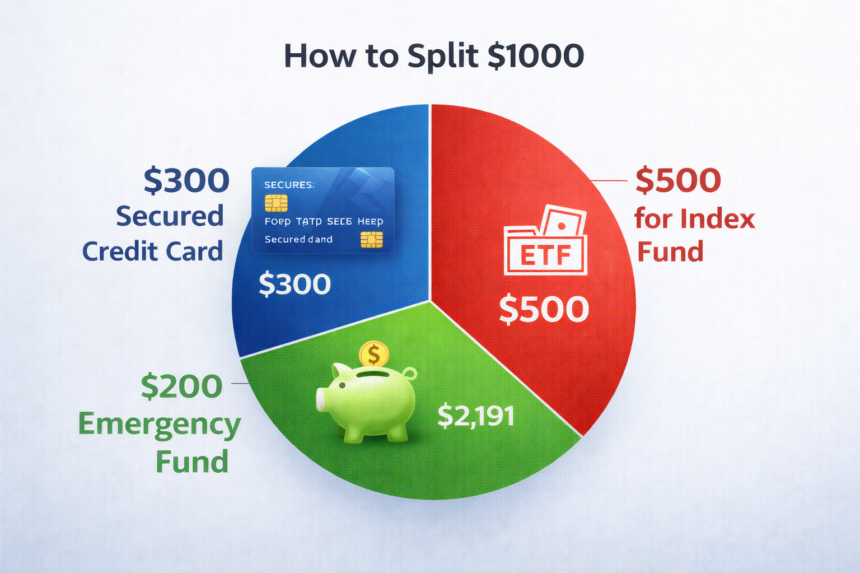

The Smart Split Strategy: How to Do Both

Okay, so you’re probably wondering: “Should I just build credit, or should I invest?” Well, why not do both? It’s honestly not that hard to split your $1000 between credit-building and investing. A lot of beginners think they have to choose one, but you can balance both. Here’s a simple plan that I’ve seen work for many people:

The “Smart Split” Strategy:

$300 for a Secured Credit Card: This will help you start building credit. You’ll need a refundable deposit, so it’s not like you’re losing money.

$200 for an Emergency Fund: Set this aside in a high-yield savings account. You never know when an emergency is going to pop up, and it’s better to be prepared.

$500 for Index Funds: Invest the rest into a low-cost S&P 500 ETF. This lets you start growing your wealth, and it doesn’t require a lot of effort on your part.

Result: After about 12 months, you’ll probably have a 700+ credit score, a small emergency fund, and a growing investment portfolio. Simple, right?

Best Investment Options for Beginners

Now that you’ve got your credit-building strategy down, let’s dive into where to put that $1000 for investing. Below is a rundown of what I consider the best options for beginners:

Investment Comparison Table

| Investment Type | Risk Level | Expected Return | Pros | Cons |

|---|---|---|---|---|

| Index Funds / ETFs | Low to Medium | 7-10% annually | Low-cost, diversified, long-term growth | Subject to market volatility |

| Robo-Advisors | Medium | 6-8% annually | Hands-off, automated, low minimums | Management fees can apply |

| High-Yield Savings | Low | 4.00% – 5.00% APY (Subject to market changes) | Safe, easily accessible | Lower returns compared to stocks |

1. Index Funds and ETFs

I know, I know—everyone says “index funds are great.” But honestly, they are. Index funds and ETFs are perfect for beginners because they’re simple and low-cost. You don’t need to pick individual stocks. You just invest in the S&P 500, and you’re invested in 500 of the largest companies in the U.S..

Where to Invest: Try Vanguard or Fidelity.

Expected Return: Historically, S&P 500 Index Funds have returned 7-10% annually.

Explore more about Index Funds.

2. Robo-Advisors

If you don’t want to think too much about your investments, robo-advisors might be a good option. They’ll automatically build a diversified portfolio for you, based on your risk tolerance. All you have to do is sign up.

Where to Invest: Consider Betterment or Wealthfront.

Expected Return: Typically 6-8% annually.

Learn more about Robo-Advisors.

3. High-Yield Savings Account

If you’re not into the stock market, a high-yield savings account (HYSA) is another option. You can earn some interest without any risk, though it’s not going to make you rich. Still, it’s a good way to keep your money safe while it earns a bit.

Where to Invest: Try Marcus by Goldman Sachs or Ally Bank.

Expected Return: Currently 4.00% – 5.00% APY (Subject to market changes).

Common Mistakes When Using a Secured Credit Card

You’re probably thinking this is all pretty straightforward, right? But here’s the thing: beginners make mistakes with secured cards all the time. I see it happen again and again. Here’s what you need to avoid:

Maxing Out Your Credit Limit: Don’t spend all of your limit. Stick to using less than 30% of your available credit. It helps keep your credit score healthy.

Missing Payments: This is a huge one. Just pay your bill on time. Set reminders or set it to auto-pay if you’re forgetful.

Not Monitoring Your Credit: Check your credit score regularly to make sure everything’s going well.

Pros and Cons of Secured Credit Cards

Pros:

Helps Build Credit: If you use it right, your credit score will improve.

Low Risk: You’re only spending the deposit, so you can’t get in over your head.

Path to Unsecured Cards: After a few months, you might be able to move to an unsecured card with a higher limit.

Cons:

Requires a Deposit: It’s your money tied up in the deposit.

Low Credit Limits: Your limit’s low at first. It might feel limiting.

Annual Fees: Some cards have annual fees. It’s usually low, but still, it’s something to watch out for.

Frequently Asked Questions

Usually, it takes about 3-6 months of responsible use to see improvements.

Sure, but try not to exceed 30% of your credit limit.

Yep, after 6-12 months, many issuers will offer you an unsecured card.

The Discover it® Secured Credit Card is popular because it offers cashback rewards and no annual fee.

You can start with $1000. Consider index funds, ETFs, or Robo-advisors.

Conclusion: Taking Action with Your $1000 Investment

It might feel like you’re just getting started, but don’t let that $1000 sit there collecting dust. Whether you’re building credit, starting an emergency fund, or diving into investments, every step counts. Just take it slow, make smart choices, and remember that financial success doesn’t happen overnight.

For more on credit-building, visit CFPB’s Credit Card Guide.

Disclosure: The information provided in this article is for educational purposes only and should not be considered as financial advice. Always conduct your own research or consult a professional financial advisor before making any investment decisions. Past performance is not indicative of future results.