A Beginner’s Guide Written by a U.S. Finance Expert

Many people believe investing is only for those who already have a lot of money. In my experience working with first-time investors across the United States, that belief stops more people from building wealth than any market crash ever has.

The truth is simple: you do not need a large amount of money to start investing. What you need is clarity, realistic expectations, and a system that works with small amounts—not against them.

This guide explains how to start investing with little money, step by step, in plain language. No hype. No shortcuts. Just practical advice you can actually follow.

Why Starting With Little Money Still Matters

One of the biggest misconceptions beginners have is that small investments “don’t matter.” That’s wrong.

What matters most in investing is time, not the starting amount.

Real-life example

I once helped a 24-year-old retail worker who started investing just $75 per month. It didn’t feel like much. But over time, consistency mattered more than the amount. Five years later, they had built discipline, confidence, and a solid base—something most people never achieve.

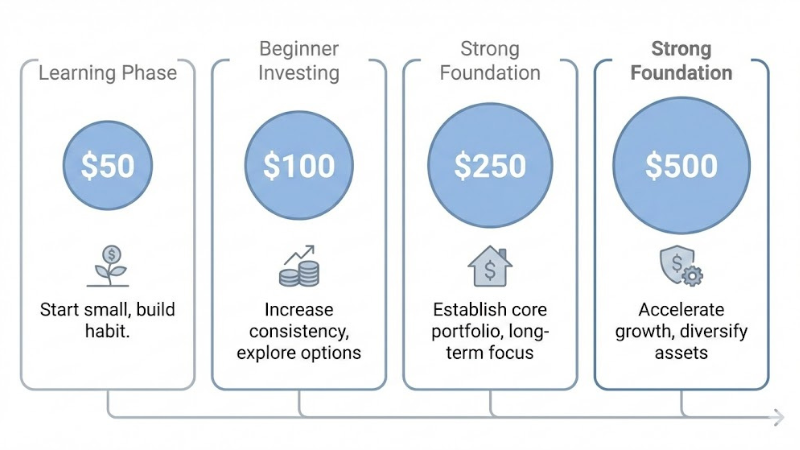

What “Little Money” Really Means (Let’s Be Honest)

Different articles avoid defining this clearly. Let’s fix that.

| Monthly Amount | What It Means in Practice |

|---|---|

| $25–$50 | Learning phase, habit building |

| $100 | Real investing begins |

| $250–$500 | Strong foundation potential |

| $1,000+ | Advanced beginner territory |

If you are in the $50–$200 range, you are exactly where most successful investors started.

Common Myths That Stop Beginners From Investing

Myth 1: “I’ll start when I earn more”

Most people never start because income always finds a way to get used elsewhere.

Myth 2: “Investing is basically gambling”

Speculation is gambling. Long-term investing is ownership.

Myth 3: “I need to pick winning stocks”

You don’t. In fact, beginners should avoid stock picking early.

Step-by-Step: How to Start Investing With Little Money

Step 1: Make Sure You’re Ready (Before Investing)

Before investing a single dollar, check these boxes:

You can pay monthly bills

You have$500–$1,000 emergency cash

You are not using credit cards for essentials

If these aren’t in place, investing can backfire emotionally and financially.

Step 2: Set a Simple Goal (Not a Big One)

Beginners fail when goals are vague.

Good beginner goals:

“Invest $100 per month for one year”

“Build my first $1,000 invested”

“Learn how markets move without panic”

Bad goals:

“Get rich fast”

“Beat the market”

Step 3: Understand Your Investment Account Options (U.S.)

This is where many articles get confusing. Let’s simplify.

| Account Type | Best For | Minimum |

|---|---|---|

| Brokerage account | General investing | $0–$100 |

| Roth IRA | Long-term retirement | $0–$100 |

| Robo-advisor | Hands-off beginners | $50–$500 |

If you’re working and earning income, a Roth IRA is often the best long-term choice.

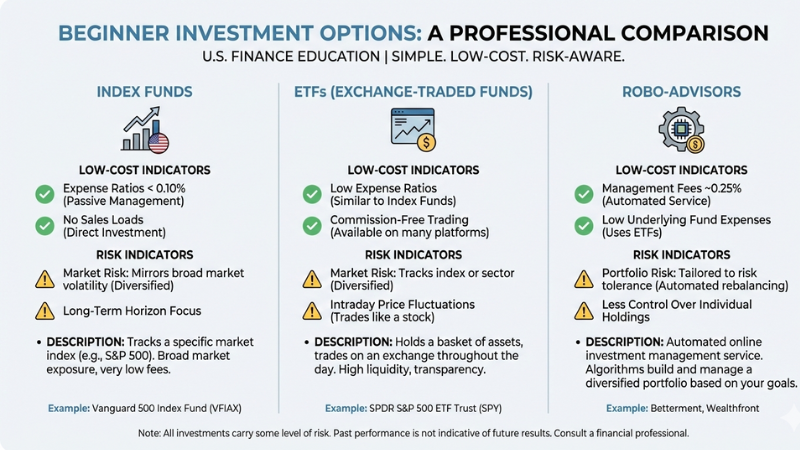

Step 4: Choose Beginner-Friendly Investments

Avoid complexity early.

Best options for small investors:

| Investment | Why It Works |

|---|---|

| Index funds | Broad market exposure |

| ETFs | Low cost, flexible |

| Robo-advisor portfolios | Automatic diversification |

What NOT to start with:

Day trading

Options

Penny stocks

Crypto speculation

These destroy beginner confidence.

Step 5: Automate Everything

In real situations, users often fail not because of bad investments—but because they stop contributing.

Automation removes emotion.

Set:

Monthly auto-deposit

Automatic investment allocation

Consistency beats intelligence here.

Real Beginner Scenarios (What Actually Works)

Scenario 1: College student with $50/month

Opens brokerage account

Buys total market ETF

Focus: learning, not returns

Scenario 2: Working adult with $200/month

Uses Roth IRA

Invests in index fund

Adds slowly with raises

Scenario 3: Side-hustler with irregular income

Keeps cash buffer

Invests only surplus

Avoids forced contributions

Pros and Cons of Starting With Little Money

Pros

Low emotional risk

Builds discipline

Teaches market behavior

Easier recovery from mistakes

Cons

Slower visible growth

Fees matter more

Requires patience

Both are normal. Growth comes later.

Comparing Beginner Investment Options

| Option | Risk | Control | Best For |

|---|---|---|---|

| Index fund | Low-Medium | Medium | Long-term growth |

| ETF | Low-Medium | High | Flexible investors |

| Robo-advisor | Low | Low | Hands-off beginners |

| Individual stocks | High | High | Later stage only |

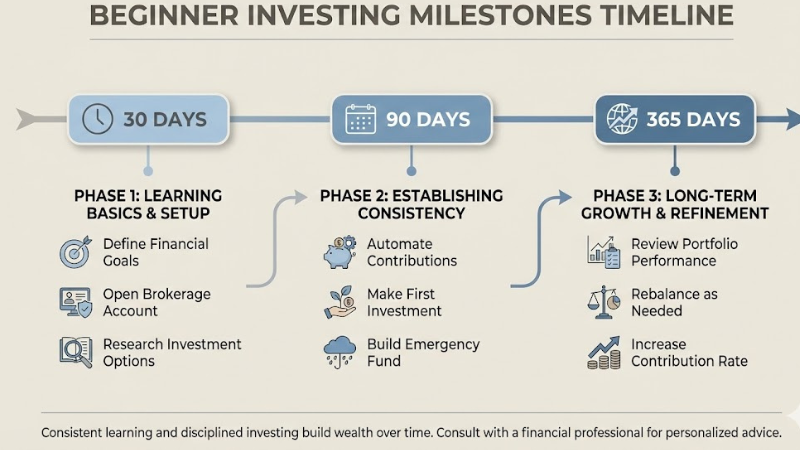

30 / 90 / 365 Day Beginner Timeline

First 30 Days

Learn terminology

Set up accounts

First investment made

First 90 Days

Market ups and downs experienced

Confidence tested

Automation proves useful

First Year

Habit solidified

Understanding improves

Returns become secondary to consistency

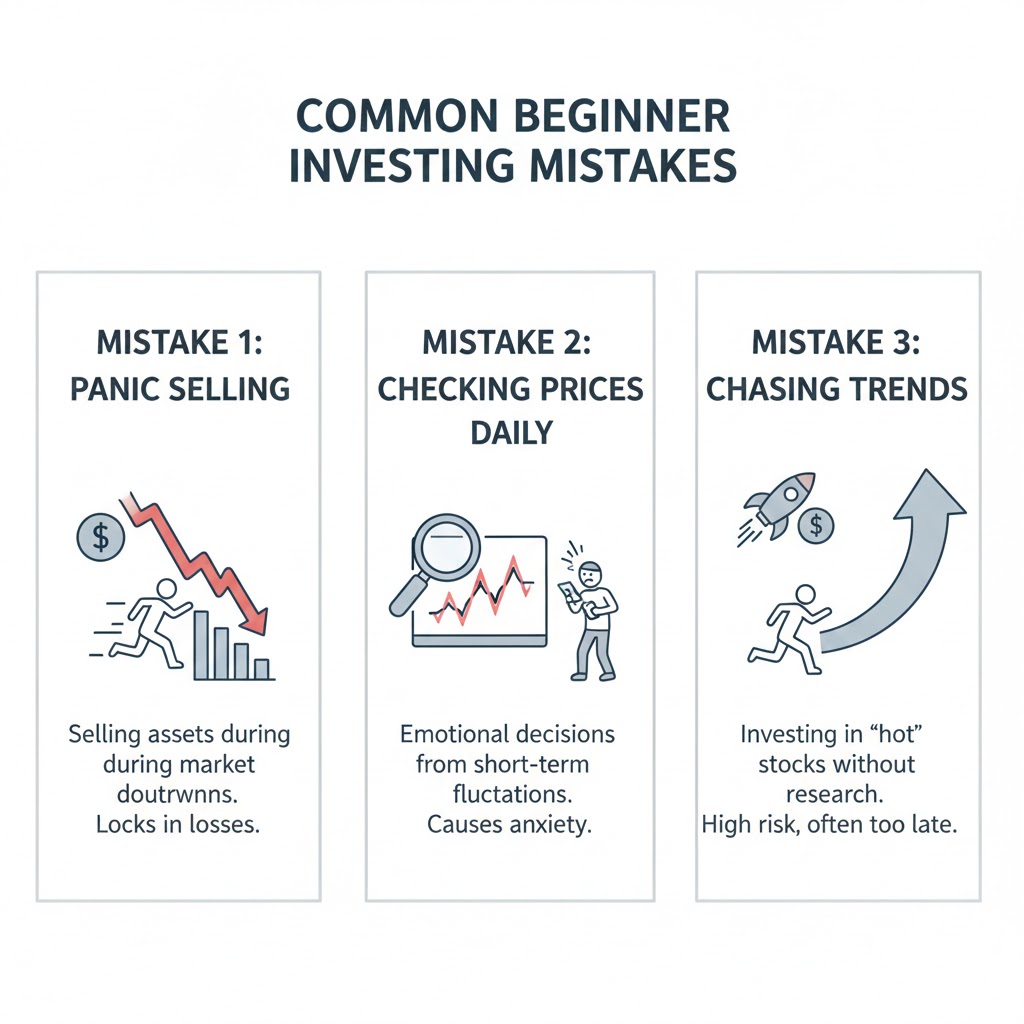

Common Beginner Mistakes (That Top Articles Don’t Warn You About)

- Watching daily market news

Panic selling during dips

Constantly switching strategies

Comparing yourself to others

Overestimating short-term returns

In my experience, staying boring is what works.

What NOT to Do When You Start Investing

Don’t invest emergency money

Don’t chase trends

Don’t copy influencers

Don’t ignore fees

Don’t expect quick results

Frequently Asked Questions

Yes. The goal is learning and consistency, not speed.

Yes—because habits compound before money does.

Not individual stocks at first. Use funds.

Months for learning. Years for meaningful growth.

Risk exists, but proper diversification controls it.

Trusted U.S. Resources

Final Thoughts

Starting to invest with little money isn’t about returns—it’s about becoming an investor.

Once you build the habit, the confidence, and the system, increasing the amount becomes easy. Waiting for the “perfect time” never works. Starting small—but starting now—does.

In my experience, the people who succeed aren’t the ones who start big. They’re the ones who start anyway.

Disclaimer:

The content on USA Harmony is for informational and educational purposes only and should not be considered financial or investment advice. Financial situations vary, and readers should consult a qualified professional before making any investment decisions.